Are sports cards the future of retail investing?

A deep dive into the next wave in consumer fintech — private asset marketplaces

The past decade has been a transformational one in financial services. The days of visiting a physical bank to open an account or apply for a loan are behind us — we now expect to do everything via a website or app. The landscape of consumer-facing brands has also changed rapidly, with startups like Chime and Robinhood taking meaningful market share from incumbents.

This evolution has been particularly noticeable in investing. Retail investors are more empowered than ever, as we’ve seen in the past few weeks with GameStop, Bitcoin, and Dogecoin. And this goes far beyond public equities and crypto — barriers to entry have started to disappear across many asset classes, as the table below illustrates.

We’ve seen three main waves of products that democratize investing:

Phase 1: Better UX for trading public assets. Consumers could trade stocks and crypto before, but these companies made it easier and cheaper with features like zero commission trades, mobile apps, and fractional shares. Robinhood and Coinbase are the two best examples of this.

Phase 2: Make private assets publicly tradable. These companies take assets that were privately owned and make it possible for anyone to buy shares. The platform is responsible for selecting, vetting, and storing the assets. Rally Rd., Otis Wealth, and Mythic Markets are examples of this.

Phase 3: P2P trading of private, digital assets. We’re in the early innings of this! These are companies enable consumers to digitally trade private assets between themselves, with the platform playing a supporting role. Examples include StarStock (sports cards), Quidd (fandom items), and Foundation & Zora (NFTs, which are basically crypto-powered collectibles — this deserves its own post, but check out CoinDesk’s primer).

Phase 3 is particularly exciting — these companies can function as true marketplaces with relatively little interference. The platform doesn’t have to acquire and IPO the assets, so the transaction volume should theoretically scale more quickly with better margins and strong network effects.

We’ll explore what this looks like through the lens of an asset class that’s breaking out — sports cards!

What‘s going on in sports cards?

eBay reported a 142% increase in trading card sales in 2020, with soccer (up 1586%) and basketball (up 373%) leading the pack. This is evident in arguably the purest measure of consumer interest — Google Trends—as well as the dozens of new podcasts and YouTube series, focused on card trading. This buzz is reaching the highest end of the market, with a new all-time record in January for the most expensive card ($5.2M!).

When we analyzed eBay GMV data in 2018, we found that sports cards & memorabilia was a top 10 category by sales volume. However, we didn’t see growth potential — we believed collecting sports cards was a hobby for older generations. Would millennials and Gen Zers be excited to hunt down cards at swap meets, mail them in for authentication, and receive a (disappointingly) small check after a “black box” evaluation process? We didn’t think so.

Clearly, we missed something — sports cards have become white-hot! What’s the appeal? A few factors have converged here:

Consumers are stuck at home and have time to invest in a new hobby. Trading cards is particularly attractive because it can generate income, especially if you already have some old cards in your attic!

The recent spike in Bitcoin has created FOMO around other asset classes — you want to get in early! Younger investors who’ve made money in crypto, sneakers, and the “meme stocks” are looking for the next opportunity, and many have moved to sports cards.

Since leaving StockX late last year, founder Josh Luber has gone all-in on trading cards (a longtime hobby)! He’s now the founder of Six Forks Kids Club, an alternative asset management company focused on trading cards.

Sports cards producers have taken advantage of the increased interest to drive up prices — they’re printing smaller runs, often stamped with serial numbers (for collectability), and offering premium autographed versions.

There’s also been a fundamental shift in what it means to trade sports cards. These cards have transformed from collectibles in plastic protectors to financial assets that you can buy & sell without physically possessing. Rally Rd. and Collectable (Phase 2 companies) hold one-off IPOs for fractional shares in high-value cards, while StarStock (Phase 3) allows for P2P digital trades — though buyers can request the physical card.

As a result, card trading has attracted sports fans who wouldn’t be caught dead at a swap meet. Many view buying a digital card as a form of gambling — they’re taking a bet that demand for a given player (or team) will increase over time. In the meantime, holding a player’s card is like drafting them to your fantasy team. You’re tracking their performance over time and invested in their success!

What are we looking for in next-gen consumer investing companies?

Sports cards are one of the first assets to be picked up by the “third wave” of fintech, but they won’t be the last! We believe that multiple $1B+ companies will be built around democratizing access to alternative assets. Here’s what we’re looking for:

1. Serves as a source of truth for asset values.

The key to a successful marketplace is liquidity. How do you recruit early users? One strategy is to become the go-to place for buyers and sellers to find a fair price (think Kelley Blue Book) by aggregating SKU-level data on things like bids, asks, clearing price, and trading volume.

StockX does a great job with sneakers. The homepage features a scrolling display of price changes, with categories like “New Highest Bid” and “New Lowest Ask.” Before buying sneakers, you’re probably going to check the price on StockX — and there’s a high likelihood you’ll end up transacting there!

2. Provides an advisor-like experience with content + education.

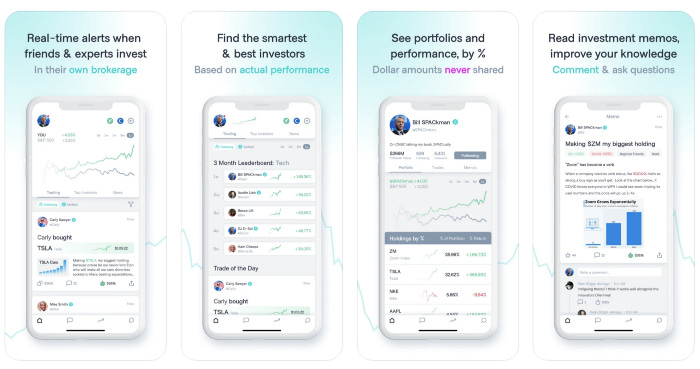

If you’ve built a liquid marketplace, consumers will come to make transactions on a weekly, monthly, or even annual basis (depending on the asset). How do you drive daily engagement and retain users over time? Provide educational content & insights on the market. Ideally, it’s in a shareable format that enables organic growth — it’s not surprising that Robinhood’s first acquisition was a newsletter (MarketSnacks).

One great example of this is Titan (screenshots below), which offers hedge-fund-like strategies to retail investors. Titan updates clients via: (1) a daily “three things” newsletter; (2) weekly videos explaining major moves; (3) monthly and quarterly reports; and (4) longer-form research pieces on stocks they are tracking or adding to the portfolio.

3. Social incentives to invest and engage with friends.

Consumer fintech products can be just as viral as social apps — think about Robinhood’s famous pre-launch waitlist! For many Gen Z and millennial consumers, investing is a “team sport.” Companies can take advantage of this with social features and gamification, like a live feed of friends’ trades and a leaderboard ranking performance. CommonStock is a good example of this — users can follow other investors, copy their trades, and talk in group chats.

Eventually, we expect that these investing platforms will create a new genre of creators. Some users will gain an audience by accurately predicting future asset prices or creating helpful content for new investors. Other users could pay to get exclusive access to their trades or even invest in a fund controlled by that creator (similar to AngelList syndicates).

4. Users can showcase their ownership or interact with the asset.

One of the benefits of owning a physical asset is showing it off to friends. How do you recreate this digitally? Exclusive content. NBA Top Shot allows consumers to buy highlight clips from games & display them via virtual collections and compilation videos — the company did $30M in sales in January! NFT companies like Foundation and Zora are reinventing the experience of being a collector of limited edition digital goods.

We’ve also seen companies get creative about what asset ownership “unlocks” in the real world. Rally Rd. investors can visit the company’s showrooms, and StarStock investors can ask for their physical cards. We expect see this to evolve — imagine a world where you invest in a musician through AmplifyX and get access to special concerts, exclusive merch, and meet-and-greets.

5. Empower next-gen investors with low (or no) minimums.

To become a breakout consumer product, an investing platform needs to be broadly accessible. Few users will be interested in an app that requires an initial commitment of $50K (or even $5K!), and even fewer will share it with their friends. Users need to be able to start small — they’ll grow their accounts over time as they gain trust in the platform and their net worth increases.

It’s crucial that small investors aren’t treated as “second class citizens” — while large investors may get more perks, all users should be able to use the core product & engage with the community. Bitwise, which manages crypto index funds, has done a great job with this. The company has a publicly-traded fund with no minimums, as well as an offshore version for accredited investors ($100k minimum) and institutions ($1M minimum).

A new class of retail investors has been mobilized, and they’re looking for investment opportunities. We’re excited to see who will ride this third wave of consumer fintech to build a category-defining company!

What are we missing? We’d love to hear about any startups building platforms around this thesis, whether for sports cards or another asset class. Comment below or DM us on Twitter!

If you’re interested in reading more from us, you can also subscribe to our weekly newsletter, Accelerated 🚀

This post was originally published on Medium.